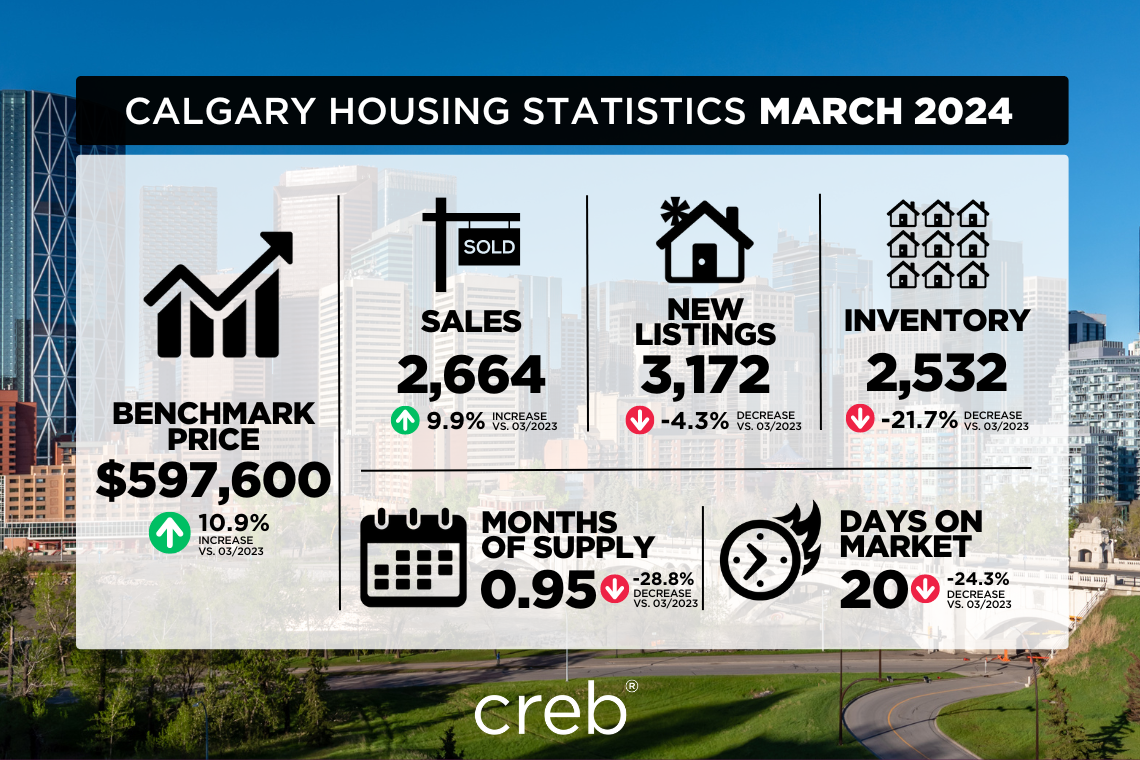

March reflects strong seller's market and price increases

City of Calgary, April 1, 2024 – March sales rose to 2,664 units, a 10 per cent year-over-year gain and much higher than long-term trends. While new listings did pick up over last month, the 3,172 units were still below what we typically see in March and not enough relative to sales to drive any change in the supply situation. In March, the sales-to-new listings ratio rose to 84 per cent, and the months of supply fell below one month.

“We have not seen March conditions this tight since 2006, which is also the last time we reported high levels of interprovincial migration and a months-of-supply below one month," said Ann-Marie Lurie, Chief Economist at CREB®. “Moreover, we are entering the third consecutive year of a market favouring the seller as the two-year spike in migration has driven up demand and contributed to the drop in re-sale and rental supply. Given supply adjustments take time, it is not a surprise that we continue to see upward pressure on home prices.”

Inventory levels have declined across properties priced below $1,000,000, with the steepest declines occurring for homes priced below $500,000. In March, there were 2,532 units in inventory, 22 per cent lower than last year and half the levels we traditionally see in March.

In March, the unadjusted total residential benchmark price rose to $597,600, a two per cent gain over last month and nearly 11 per cent higher than last year. Prices have increased across all property types, with the most significant year-over-year gains occurring for the relatively more affordable row and apartment-style homes.

Detached

Detached home sales rose in March but were likely limited by the level of new listings coming onto the market. New listings in March were 1,386 units, compared to the 1,151 sales, causing the sales-to-new listings ratio to rise to 83 per cent. Inventories also remained relatively stable compared to last month but were 24 per cent lower than last year’s levels and nearly 60 per cent lower than long-term trends for March. Inventory levels dropped across all price ranges, but the most significant fall was in the lower price point. Overall, 71 per cent of the available inventory in March was priced above $700,000.

Low inventories compared to sales caused the months of supply to drop below one month, driving further price gains. The unadjusted detached benchmark price rose to $739,700, a monthly gain of nearly three per cent and a year-over-year gain of 14 per cent. The largest year-over-year gains occurred in the most affordable North East and East districts.

Semi-Detached

Supply availability continues to weigh on the semi-detached sector of the market. In March, 260 new listings were met with 250 sales, causing the sale-to-new listings ratio to rise to 96 per cent. This prevented inventories from improving, and the months of supply dropped below one month. Inventory declines have been driven mainly by properties priced below $600,000.

Limited supply and growing demand drove further price gains in March. The unadjusted benchmark price reached $658,000, nearly three per cent higher than last month and a 14 per cent gain over last March. Prices rose across all districts in the city, with year-over-year gains ranging from a low of 11 per cent in the highest-priced area of the City Centre to 25 per cent in the lowest-priced market in the East district.

Row

Both sales and new listings rose in March. However, with 536 new listings and 449 sales, the sales-to-new listings ratio rose to 84 per cent, preventing any significant monthly change in inventory levels. With 355 units available, inventory levels were 12 per cent below last year’s and 53 per cent below long-term trends for March. The decline in inventory levels was driven by properties priced below $400,000, as inventory levels rose 35 per cent for units priced above $400,000.

The unadjusted benchmark price trended up in March, reaching $448,700, a monthly gain of nearly three per cent and over 20 per cent higher than levels reported at this time last year. The higher-priced City Centre reported the slowest growth in benchmark prices, with the highest growth reported in the city's most affordable districts.

Apartment Condominium

Sales in March reached 814 units, contributing to the first quarter’s record-high sales of 1,940 units, nearly 31 per cent higher than last year. New listings also improved throughout the first three months of the year, but with a March sales-to-new-listings ratio of 82 per cent and a months-of-supply of one month, conditions favoured apartment condominium sellers.

Demand for lower-priced homes has supported the growth of apartment-style properties, but the tight conditions have also contributed to further price gains. In March, the benchmark prices reached $337,700, over two per cent higher than last month and 17 per cent higher than levels reported last March.

REGIONAL MARKET FACTS

Airdrie

March reported 203 sales and 218 new listings. While both new listings and sales improved, with a sales-to-new listings ratio of 93 per cent, inventory levels were 22 per cent below last year and 56 per cent below typical March levels.

With less than one month of supply, it is not surprising that we continue to see upward pressure on home prices. In March, the benchmark price reached $540,400, a monthly gain of two per cent and a year-over-year increase of over nine per cent. Prices improved across all property types, with stronger year-over-year gains for the relatively lower-priced row and apartment-style products.

Cochrane

Following a slower start to the year, sales in March rose to nearly the same level of new listings coming onto the market, pushing the sales-to-new listings ratio up to 99 per cent. This also contributed to further declines in inventory levels, and the months of supply dropped to just over one month.

As of March, the total residential benchmark price reached $555,300, a monthly gain of over one per cent and a year-over-year increase of nearly 12 per cent. Prices rose across all property types, and detached prices pushed above $650,000 for the first time.

Okotoks

Okotoks continues to struggle with supply as the 71 new listings that came on the market this month were met with 65 sales, preventing any improvement in inventory levels. There were only 54 units available in March, a year-over-year decline of 10 per cent and nearly 70 per cent below long-term trends for the month.

Limited supply and strong sales caused the months of supply to fall below one month, and March was the lowest March reported since 2006. Persistently tight conditions drove further price growth this month, as the total residential benchmark price rose to $610,700, a monthly gain of one per cent and a year-over-year increase of nine per cent. Prices have been rising for all property types, with the most significant year-over-year gains occurring for semi-detached and row properties.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

.png?cc=1712161635251)

.png?cc=1706999295758)